Social Security checks are not projected to stop in 2032. The danger is different. The retirement trust fund is projected to run out of reserves, and the money still coming into the program would not cover every scheduled retirement and survivor benefit.

The Congressional Budget Office projects that the Old-Age and Survivors Insurance Trust Fund will be exhausted in fiscal year 2032. Under the payable-benefits scenario CBO analyzed, retirement and survivor benefits would be reduced by 7% in 2032 and by an average of 28% per year from 2033 through 2036.

The 2026 Social Security Trustees Report points to the same danger window. The Trustees project that the OASI fund will be depleted in the fourth quarter of 2032. At that point, incoming revenue would cover 78% of scheduled OASI benefits.

For retirees, survivors and people nearing retirement, the warning is no longer a distant policy chart. It is a deadline inside the next decade.

The 2032 Warning Is About Retirement And Survivor Benefits

Social Security has separate trust funds. The OASI fund pays retirement and survivor benefits. The Disability Insurance Trust Fund pays disability benefits.

CBO’s 2032 warning is focused on the OASI fund. That includes retired workers, spouses, eligible dependents and survivors of deceased workers.

The Disability Insurance fund is in better shape. The 2026 Trustees Report says the DI fund is projected to remain positive throughout the 75-year projection period.

| Trust Fund | Benefits Paid | 2026 Outlook |

| OASI | Retirement benefits, spouse benefits, eligible dependents and survivor benefits | CBO and Trustees project depletion in 2032 |

| DI | Disability benefits and related family benefits | Trustees project reserves remain positive through the 75-year period |

| Combined OASDI | Illustrative combined view of retirement, survivor and disability funds | Trustees project depletion in 2034 with 83% of scheduled benefits payable |

Headlines often mix the separate OASI date with the combined OASDI date. That is why readers may see 2032, 2033 or 2034 in different reports.

CBO Projects A 7% Cut In 2032 And Deeper Cuts Afterward

CBO analyzed a scenario in which OASI benefits are limited to dedicated Social Security revenue once the trust fund is exhausted.

Under that scenario, benefits fall 7% in 2032. The reduction grows after the trust fund is gone for a full year. CBO estimates average annual benefit cuts of 28% from 2033 through 2036.

| Period | CBO Projection | Effect On Benefits |

| 2032 | 7% reduction | First projected cut after the OASI trust fund reaches exhaustion |

| 2033 through 2036 | Average 28% annual reduction | Much larger cuts if benefits are limited to dedicated revenue |

| 2032 through 2036 | $2.7 trillion total reduction | Scheduled benefits that would not be paid in the payable-benefits scenario |

A retiree receiving $2,000 a month would lose about $140 a month under a 7% cut. A 28% cut would reduce that same check by about $560 a month.

CBO also notes that current law does not give a detailed payment method for trust fund exhaustion. Congress has never allowed Social Security to reach that point, so the exact administrative process remains unresolved.

The Trustees Also Put The Retirement Fund Deadline In 2032

The 2026 Trustees Report projects that the OASI Trust Fund will be depleted in the fourth quarter of 2032. After that, continuing income would cover 78% of scheduled OASI benefits.

The combined OASI and DI funds are projected to pay full scheduled benefits until 2034. After combined depletion, 83% of scheduled benefits would be payable.

The two reports do not use the same methods, but they now point to the same basic retirement-fund deadline. The OASI fund is projected to run short in 2032 unless Congress changes the law.

| Measure | CBO | 2026 Trustees Report |

| OASI retirement and survivor fund | Exhausted in fiscal year 2032 | Depleted in Q4 2032 |

| Benefits payable after OASI depletion | Benefits limited to dedicated revenue under the scenario | 78% of scheduled benefits payable |

| Combined OASDI funds | Exhausted in 2033 if combined | Depleted in Q3 2034 |

| Benefits payable after combined depletion | Separate CBO projection | 83% of scheduled benefits payable |

The Trustees also reported that Social Security paid $1.60 trillion in benefits in 2025 and had 70 million beneficiaries at the end of the year. Program costs exceeded total income in 2025, and the long-range actuarial deficit worsened from the prior report.

Payroll Taxes Would Continue But They Would Not Cover Full Benefits

Social Security is financed mainly through payroll taxes. CBO says payroll taxes account for 96% of Social Security revenue. The program also receives revenue from income taxes on benefits and interest on trust fund holdings.

The 2026 taxable wage cap is $184,500. Workers and employers each pay half of the 12.4% payroll tax. Self-employed workers pay the full amount.

The funding problem comes from the gap between scheduled benefits and incoming revenue. More retirees are collecting benefits. People are living longer. Revenue does not rise fast enough to keep full scheduled payments going after the trust fund reserves are depleted.

That is why the phrase “Social Security is going bankrupt” can mislead readers. The program would still collect taxes. The issue is that tax income would not pay the full benefits promised under current law.

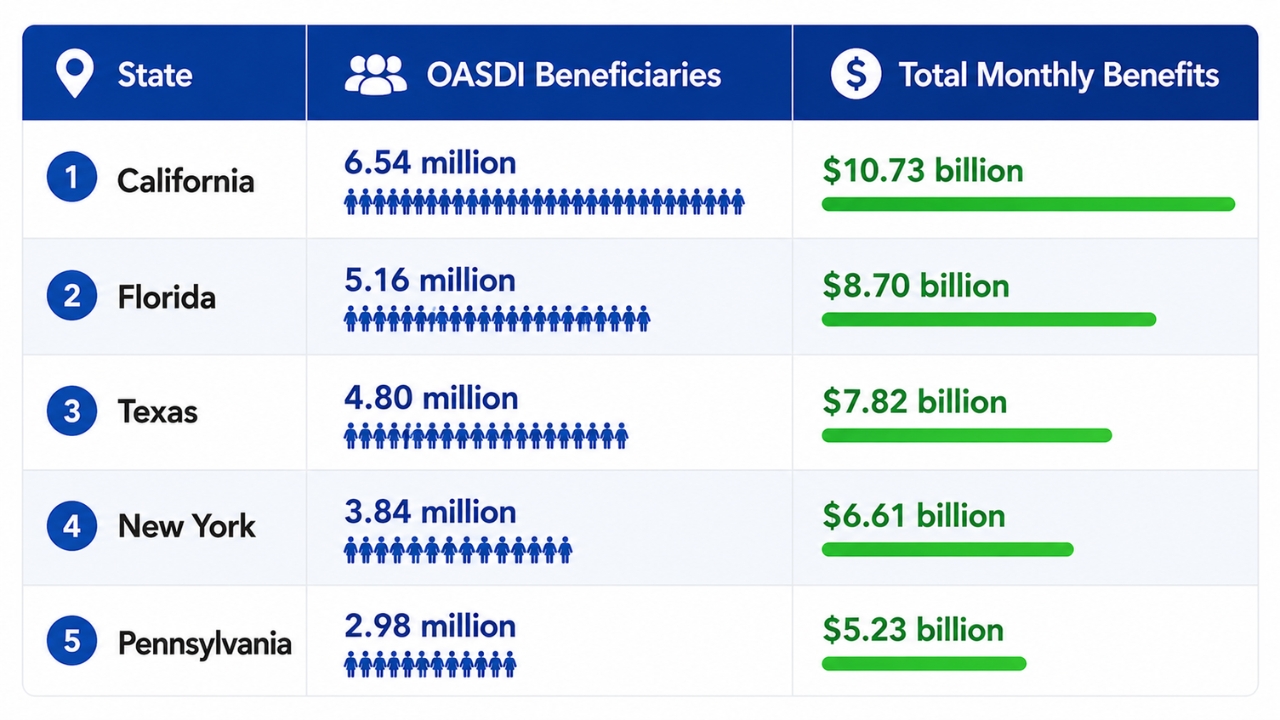

The States With The Most Beneficiaries Have The Largest Exposure

SSA state data show 68.46 million OASDI beneficiaries in current-payment status in December 2024. California had the largest number of beneficiaries, followed by Florida, Texas, New York and Pennsylvania.

| State | OASDI Beneficiaries In December 2024 | Why The Exposure Is Large |

| California | 6,544,000 | Largest beneficiary population in the country |

| Florida | 5,161,992 | Large retiree population and heavy dependence on monthly benefits |

| Texas | 4,802,392 | Large population and broad retirement, disability and survivor benefit base |

| New York | 3,838,030 | Large beneficiary count in a high-cost state |

| Pennsylvania | 2,981,684 | Older population and large retirement benefit base |

| Ohio | 2,507,421 | High number of retired workers, disabled workers and survivors |

| Illinois | 2,360,590 | Large beneficiary base across retirement and disability categories |

| Michigan | 2,339,826 | Large older population and strong reliance on retirement benefits |

| North Carolina | 2,329,477 | Growing state with a large retiree base |

| Georgia | 2,023,789 | More than 2 million beneficiaries receiving current payments |

A national cut would not be calculated state by state. The state table shows where the biggest populations are exposed.

The effect would still differ by place. A smaller check in a high-rent city creates a different problem from a smaller check in a lower-cost county. A retiree with savings has more room than a widow relying mainly on Social Security.

A Cut Would Reach Household Budgets Fast

Social Security is monthly income. That is why even a smaller reduction can cause real damage.

For many households, the check pays for rent, groceries, utilities, Medicare premiums, prescriptions, property taxes and credit card minimums. A 7% cut can force one bill to move behind another. A 28% cut can change where someone lives, what medical care they delay and how much family help they need.

The effect would also reach local economies. Social Security checks flow into grocery stores, pharmacies, landlords, clinics, gas stations and small businesses. A national benefit cut would remove cash from communities every month.

Readers tracking payment timing can also review our guide to Social Security payment schedules, since even normal payment dates can shape household cash flow.

Congress Has Few Easy Choices Left

Congress can still prevent the projected reductions. The tools are known. The politics are the obstacle.

Lawmakers can raise revenue, reduce scheduled benefits, change retirement age rules, shift money from other parts of the federal budget or combine smaller changes. Every option creates winners, losers and campaign attacks.

| Policy Option | How It Helps The Program | Main Fight |

| Raise the payroll tax rate | Brings in more dedicated revenue from workers and employers | Workers take home less pay, and employers face higher labor costs |

| Raise or remove the taxable wage cap | Taxes more earnings above the current cap | Higher earners pay more, and opponents call it a tax increase |

| Slow future benefit growth | Reduces long-term scheduled costs | Future retirees receive less than current formulas promise |

| Raise the full retirement age | Reduces lifetime benefits for many workers | Physically demanding jobs and shorter life expectancy make the change harsher for some groups |

| Change taxation of benefits | Can increase revenue from higher-income beneficiaries | Retirees may experience it as another cut |

| Use general revenue | Can protect benefits without relying only on payroll taxes | Adds pressure to the wider federal budget |

| Use a mixed package | Spreads changes across taxes, benefits and timing | Requires bipartisan votes that Congress has avoided for years |

Our earlier report on Social Security retirement age proposals explains why raising the full retirement age functions like a lifetime benefit reduction for many workers.

Our coverage of the Social Security COLA projection also shows the other side of the pressure. Annual benefit increases help retirees deal with current prices, but they do not solve the long-term financing gap. Also, there is a plan to make COLA flat-rate in the future.

Also, there will be 3 major changes in 2027, the Social Security Administration will announce them in October.

The New Commission Proposal Shows Washington Knows The Deadline Is Close

Reps. Tom Cole and Tom Suozzi introduced the Bipartisan Social Security Commission Act of 2026, also listed as H.R. 9187.

The proposal would create a 13-member commission made up of lawmakers and outside experts. The group would be asked to develop legislation to restore long-term Social Security solvency. The plan would then move through a faster congressional process.

A commission does not fix Social Security by itself. It can give lawmakers a structure for negotiation, but Congress still has to vote for tax changes, benefit changes or both.

The risk is delay dressed up as process. The opportunity is that a commission could give both parties a way to negotiate before the 2032 deadline forces a rushed deal.

What Current Retirees Should Do Before 2032

Current retirees should not assume their checks will vanish. They also should not build a budget on the belief that Congress will act before the last minute.

The safer approach is to measure how much of the household budget depends on Social Security and how much room exists if benefits are reduced.

- Check how much of monthly spending depends on Social Security.

- Build cash reserves if income allows.

- Review rent, mortgage, property tax and insurance costs before retirement income tightens.

- Pay down high-interest debt where possible.

- Avoid early claiming decisions based only on political fear.

- Watch official SSA and CBO updates instead of campaign claims.

- Keep Medicare, tax and Social Security planning connected, not separate.

Workers in their 50s and early 60s face a different planning problem. A late congressional fix could affect claiming age, payroll taxes, future benefit growth or the taxable wage cap during their final working years.

What The 2032 Deadline Does Not Say

The 2032 projection does not say Social Security is ending. It does not say workers should stop paying attention to the program. It does not say every beneficiary will definitely lose the same amount.

It says the retirement trust fund is projected to run out of reserves, and scheduled benefits would exceed dedicated revenue.

Congress can still change that path. The later it acts, the harder it becomes to avoid sharper changes.

The Real Risk Is Delay

The 2026 reports leave little room for a comforting reading. CBO and the Trustees both place the retirement fund deadline in 2032.

A 7% reduction in the first CBO year would already be painful for households living close to the edge. The average 28% annual cuts projected from 2033 through 2036 would force a much deeper reset for retirees, survivors and families who rely on monthly benefits.

Social Security can still be repaired before those cuts arrive. The question is not whether Congress knows the numbers. The question is how long lawmakers will wait before they make voters face the trade-offs.