Divorce in America has changed.

Overall, divorce has declined in recent decades, but divorce among older adults has moved in the opposite direction.

Gray divorce means divorce involving adults aged 50 and older. Its growth now affects retirement, housing, estate plans, inheritance, and financial security.

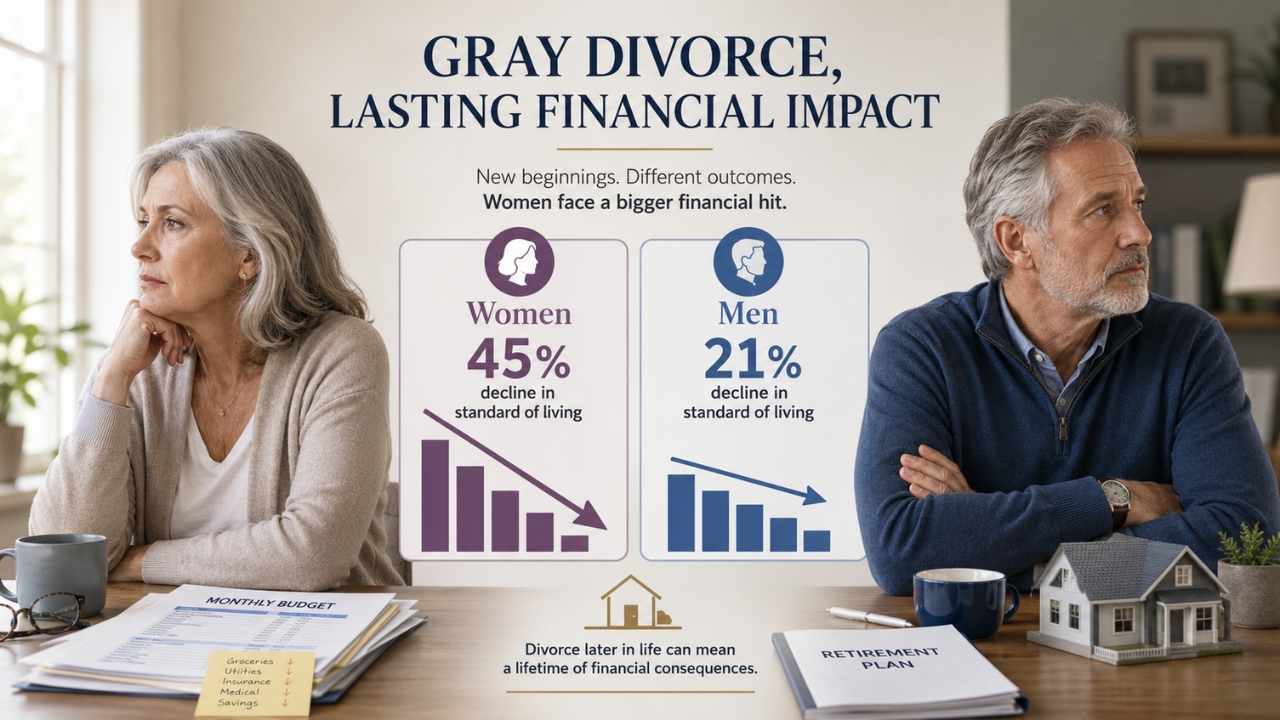

Baby Boomers are central to the trend. Their late-life divorces are splitting retirement savings, changing estate plans, and redirecting inheritance that families may have expected to pass to adult children or grandchildren. Lower stigma has also made late-life divorce more acceptable. For many Baby Boomers, divorce became more common during adulthood, so leaving a marriage after 50 no longer carries the same social weight it once did. Greater financial independence matters too, especially for women. For couples who have already agreed on the main terms, online tools such as divorce in Michigan with YourForms can help prepare state-specific uncontested divorce paperwork, but financial, retirement, and estate issues still need careful review. More women in this generation worked, earned income, and gained more control over money than many women in earlier generations. Empty-nest years can expose weak marriages. After children leave home and work slows down, some couples realize their relationship depended more on routine than emotional connection. Some experts call these relationships “empty shell marriages.” A couple may stay legally married, but the relationship lacks closeness, satisfaction, or affection. For some older adults, retirement becomes a moment to ask if their marriage still supports their quality of life. Younger adults are divorcing less often than older adults. Divorce rates among people in their 20s and 30s have declined since 1990, while divorce rates among adults over 50 have increased. Later marriage helps explain part of the difference. Younger Americans often marry later, and those who do marry are more likely to have a stronger education and financial stability, both linked with lower divorce risk. Baby Boomers have a different pattern. Many have lived through decades of higher divorce, remarriage, and changing expectations around marriage. Prior divorce and remarriage raise the chance of later divorce. Second and later marriages often carry more financial and family pressure, especially when adult children, stepchildren, pensions, homes, and inheritance plans are involved. Gray divorce also includes older members of Generation X, but Baby Boomers are having the biggest current impact on retirement planning because many are already retired or close to it. Retirement plans are often built around one shared household. Gray divorce breaks that plan apart. Savings that once supported one couple must now support two homes, two budgets, two healthcare plans, and sometimes two different retirement timelines. Older couples have less time to rebuild wealth. Peak earning years may be over, and some spouses may already be retired. Major assets in gray divorce often include: For older couples, the biggest asset may not be the house. It may be the retirement account. That matters because retirement assets can involve taxes, withdrawal rules, required minimum distributions, and long-term income planning. Housing also becomes harder. One home may need to become two. Selling can create cash, but buying or renting separately can raise monthly costs. A single-person household usually costs much more than half of a two-person household. Each person may need to pay separately for housing, utilities, transportation, insurance, food, and healthcare. Late-life divorce can force a full reset of lifestyle, spending, retirement timing, housing, taxes, and long-term care planning. Gray divorce can damage both spouses financially, but women often face larger losses. Many older women had career interruptions because of caregiving, child-rearing, or support for a spouse’s career. That can mean lower lifetime earnings, smaller retirement accounts, weaker pension access, and lower Social Security benefits. Research cited on gray divorce found a major gap: Some women also enter divorce without a clear view of household finances. A spouse may have handled investments, taxes, insurance, loans, and retirement accounts for decades. After a divorce, they may need to quickly learn about account values, credit, taxes, legal documents, and withdrawal rules. Independent credit can also be a problem. A woman who relies on joint accounts or a spouse’s income may face difficulty renting, qualifying for a mortgage, or opening credit lines. Longer life expectancy adds pressure. Women often live longer than men, so smaller retirement assets may need to last more years. Social Security can become a key issue in gray divorce. Rules for divorced spouses can be confusing, and poor timing can reduce income. Some divorced spouses may qualify for benefits based on a former spouse’s earnings record. In many cases, the marriage must have lasted at least 10 years. A divorced spouse may need to compare benefits based on personal earnings with benefits based on a former spouse’s record. Social Security should be reviewed before a settlement is final, especially when one spouse has limited retirement savings or a weaker earnings history. Gray divorce usually requires a full estate plan review. Wills, trusts, powers of attorney, healthcare directives, retirement account beneficiaries, life insurance beneficiaries, and 401(k) designations may all need updates. Changing a will is not enough. Retirement accounts and life insurance policies often pass by beneficiary designation, not by will. That creates risk. An ex-spouse could still receive a major account or life insurance payout if the paperwork was never changed. One reported case involved a client who learned after her husband died that he had not changed the beneficiary on his life insurance policy. Hundreds of thousands of dollars went to his ex-wife. Taxes can also distort a divorce settlement. Two assets may look equal on paper but carry very different tax costs. Another reported case involved a woman who later realized her “equal” split was not equal because she received accounts with a higher tax burden than her husband. Powers of attorney and healthcare directives also need attention. Without updates, an ex-spouse may still have authority over medical or financial decisions. A divorce settlement does not automatically fix an estate plan. Every document and account must be checked separately. Baby Boomers are changing both divorce and retirement. Longer lives, reduced stigma, shifting gender roles, and higher expectations for emotional fulfillment have made late-life divorce more common. Impact reaches spouses, adult children, heirs, financial planners, courts, and retirement systems. Late-life divorce is no longer rare. Retirement planning now has to account for the chance that “till death do us part” may end decades before death.

Why Gray Divorce Is Rising

Retirement can last 20 to 30 years or more, so many older adults do not want to spend those years in an unhappy or emotionally distant marriage.

Baby Boomers Are Divorcing Against the Broader National Trend

Retirement Plans Built for One Household Must Now Support Two

Women Often Face the Steepest Financial Consequences

Social Security Becomes a Major Planning Issue

Estate Plans, Beneficiaries, and Inheritance Get Complicated

FAQs

Closing Thoughts