Medicare Part B plays a major role in helping older Americans pay for outpatient medical care and physician services.

CMS announced that the Medicare Part B annual deductible will rise to $283 in 2026, compared to $257 in 2025.

Standard monthly premiums will also increase to $202.90, up from $185.00.

Nearly all Medicare beneficiaries will feel the impact of these higher costs as healthcare spending continues to climb across the United States.

CMS linked the increase to rising spending tied to outpatient hospital care, physician-administered medications, and growing use of medical services among older adults.

Higher provider reimbursement rates and ongoing healthcare inflation also contributed to the adjustment.

What Is Medicare Part B?

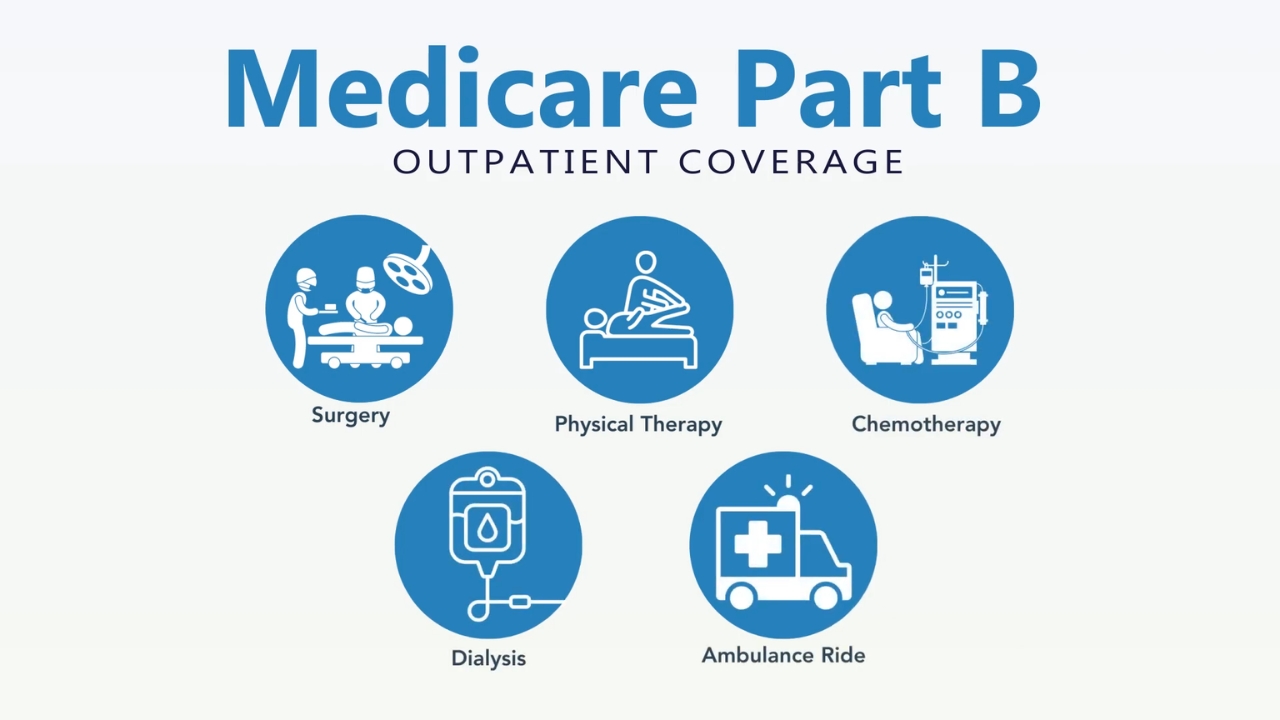

Medicare Part B provides coverage for outpatient medical care and preventive healthcare services for eligible beneficiaries across the United States.

Many seniors depend on Part B to help lower medical expenses tied to doctor visits, diagnostic testing, and ongoing treatment for chronic health conditions.

Outpatient healthcare costs can quickly add up without supplemental coverage, especially for individuals requiring frequent medical attention throughout the year.

Part B operates as one of the main components of Original Medicare.

Coverage focuses primarily on medically necessary outpatient treatment rather than hospital admission care covered under Medicare Part A.

Millions of Americans enrolled in Medicare use Part B benefits regularly for preventive screenings, specialist consultations, and medical monitoring.

Preventive care remains an important part of Part B coverage because early detection often helps reduce serious medical complications later in life. Medicare fully covers many preventive services when beneficiaries meet eligibility requirements and healthcare providers accept Medicare assignment. Older adults managing diabetes, heart disease, arthritis, cancer, and other chronic conditions frequently rely on Part B for regular appointments and treatment plans. Access to outpatient care helps many beneficiaries avoid unnecessary hospital admissions and maintain better long-term health outcomes. Beneficiaries must pay the deductible amount before Medicare begins covering most outpatient medical expenses. Medicare generally covers 80% of approved healthcare costs after the deductible requirement is satisfied. Beneficiaries become responsible for the remaining 20% coinsurance amount tied to approved services and treatments. Common healthcare expenses subject to coinsurance include specialist consultations, MRI and CT imaging scans, outpatient procedures, physical therapy appointments, and durable medical equipment such as a rollator walker. Deductible amounts reset at the beginning of every new calendar year. Beneficiaries receiving medical treatment early in the year may notice larger out-of-pocket expenses until the deductible requirement is fully met. Certain preventive healthcare services do not require deductible payments or coinsurance costs when Medicare approves the treatment at no additional charge. Annual wellness visits, select screenings, and preventive vaccines often fall into that category. Healthcare spending growth continues pushing Medicare costs higher, entering 2026. CMS announced increases affecting both standard monthly premiums and annual deductibles for Medicare Part B beneficiaries nationwide. Rising outpatient care utilization, increasing provider reimbursement rates, and continued growth in physician-administered drug spending all contributed to the updated cost structure. Many seniors will notice larger monthly healthcare expenses beginning in January 2026. Standard Medicare Part B premiums will increase to $202.90 per month during 2026. Monthly premiums totaled $185.00 in 2025, representing a $17.90 increase. Higher monthly premiums can create financial strain for retirees living on fixed incomes. Many beneficiaries already dedicate a large share of retirement income toward healthcare expenses, prescription medications, and supplemental insurance coverage. Outpatient care spending continues to increase as medical providers shift more treatments away from inpatient hospital settings. Advanced therapies and same-day procedures now occur more frequently in outpatient environments, increasing pressure on Medicare Part B funding. Annual Medicare Part B deductibles will rise to $283 during 2026 compared to $257 in 2025. Total growth equals $26 year over year, representing approximately a 10.1% increase. Recent deductible adjustments had smaller increases in many prior years. Current changes indicate continued inflation pressure across the healthcare industry and rising costs tied to medical treatment nationwide. Beneficiaries receiving frequent outpatient care may reach the deductible amount quickly during the year. Seniors requiring specialist visits, laboratory testing, imaging scans, or outpatient therapies often experience higher yearly healthcare expenses due to coinsurance obligations after the deductible is met. Coinsurance costs remain an important financial responsibility under Medicare Part B. Medicare generally pays 80% of approved outpatient healthcare expenses after beneficiaries satisfy the annual deductible. Beneficiaries must pay the remaining 20% portion tied to approved services and treatments. Out-of-pocket expenses can rise significantly for individuals requiring extensive outpatient care or expensive medical equipment. Supplemental Medicare insurance plans may help reduce coinsurance expenses for some beneficiaries. Medigap coverage often assists with costs tied to outpatient treatment and physician services not fully covered under Original Medicare. Higher-income Medicare beneficiaries will continue paying larger monthly premiums under Income-Related Monthly Adjustment Amount guidelines during 2026. IRMAA applies to individuals earning more than $109,000 annually and married couples filing jointly with income above $218,000. Premium increases tied to IRMAA vary depending on income levels reported on federal tax returns filed two years earlier. Beneficiaries experiencing major income increases could see substantially larger Part B premiums. Highest-income beneficiaries may pay more than $600 per month for Medicare Part B coverage. Premium adjustments can significantly increase total yearly healthcare costs for retirees with larger investment income, retirement account withdrawals, or employment earnings. Income thresholds tied to IRMAA continue affecting more retirees as retirement savings and investment income increase nationwide. Some beneficiaries nearing threshold limits may experience premium increases after relatively modest income growth. Healthcare inflation and growing outpatient care demand continue to increase Medicare spending projections across the country. CMS attributed the 2026 premium and deductible increases to multiple healthcare cost pressures affecting Medicare Part B funding. Physician-administered prescription drugs remain one of the largest contributors to rising Medicare spending. Specialty medications used for cancer treatment, autoimmune diseases, and chronic health conditions often carry extremely high costs. Longer life expectancy also contributes to continued Medicare spending growth. Older adults now receive medical treatment for longer periods compared to previous generations, increasing demand for outpatient monitoring and chronic disease management. Medical inflation continues to rise faster than general inflation in several healthcare categories. Healthcare labor shortages, increased pharmaceutical expenses, and growing demand for specialized care continue to affect Medicare funding projections entering 2026. Medicare premiums are set to increase for 2026, putting a dent in retirees’ Social Security checks. 2026 monthly Part B premiums will climb to $202.90, an increase of nearly 10% from this year. https://t.co/OLYHJnMmYH — Yahoo Finance (@YahooFinance) November 19, 2025 Medicare Part B costs will increase again in 2026 as healthcare spending and outpatient service demand continue rising nationwide. Annual deductibles will climb to $283 while standard monthly premiums will increase to $202.90. CMS stated that higher costs tied to outpatient treatment, physician-administered drugs, and provider reimbursement rates played major roles in the updated pricing structure. Federal scrutiny around healthcare spending has also intensified after Washington paused $1.3 billion in California Medicaid payments over fraud concerns tied to reimbursement oversight. Medicare beneficiaries should review healthcare budgets carefully and prepare for potentially higher out-of-pocket medical expenses during 2026.

How the Part B Deductible Works

Annual deductibles represent one of the first out-of-pocket expenses beneficiaries face each calendar year under Medicare Part B.2026 Medicare Part B Costs at a Glance

New Standard Monthly Premium

New Annual Deductible

Coinsurance Responsibilities

Income-Related Monthly Adjustment Amounts

Why Medicare Part B Costs Are Increasing

FAQs

The Bottom Line