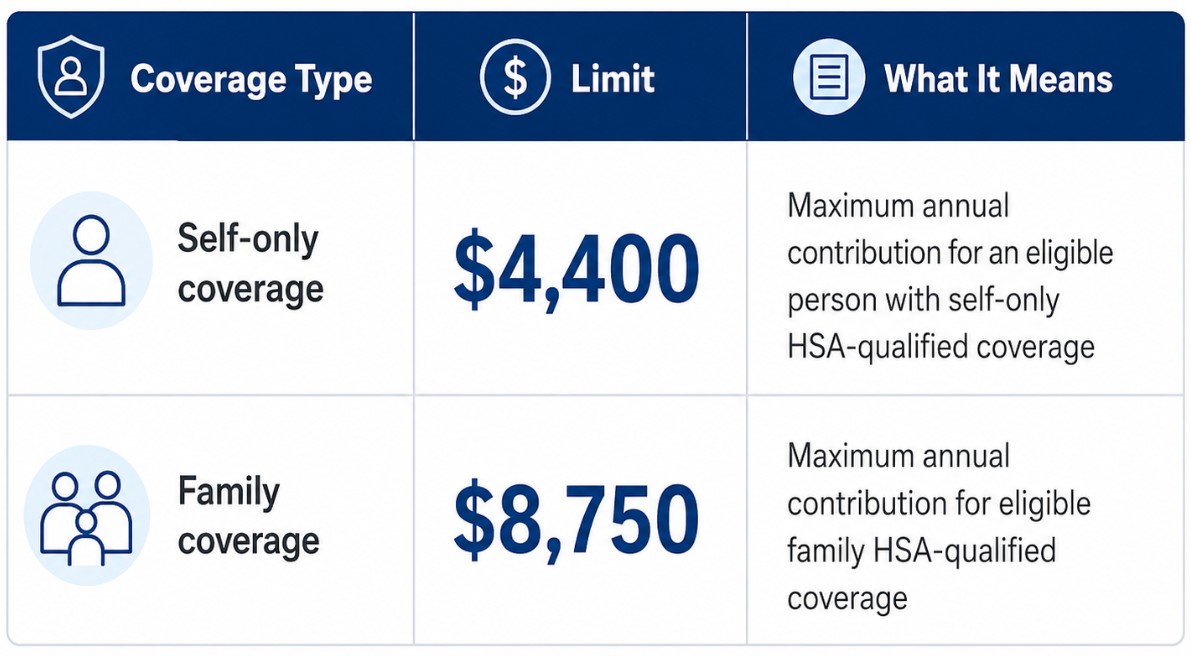

The IRS set the 2026 HSA contribution limit at $4,400 for self-only coverage and $8,750 for family coverage. Account holders age 55 or older can add a $1,000 catch-up contribution if they remain HSA-eligible.

For people using a Health Savings Account, the main question is not only how much can be contributed. The rules also depend on the health plan, employer deposits, family coverage, Medicare enrollment, spouse catch-up contributions and the deadline for making 2026 contributions.

The 2026 rules also bring wider HSA access for certain Bronze and Catastrophic health plans, plus updated treatment for telehealth and direct primary care arrangements. That makes the account more relevant for workers, families, self-employed people and anyone buying eligible individual coverage.

The official limit comes from IRS Revenue Procedure 2025-19. Consumer-facing summaries from Fidelity and Empower list the same 2026 numbers: $4,400 for self-only coverage, $8,750 for family coverage and a $1,000 catch-up amount for eligible account holders age 55 and older.

What Are the HSA Contribution Limits in 2026?

The annual HSA contribution limit includes every deposit made for the year. Payroll deductions, direct contributions, employer money, wellness incentives and third-party deposits all count toward the same IRS cap.

Coverage Or Situation

2026 HSA Contribution Limit

What It Means

Self-only coverage

$4,400

Maximum annual contribution for an eligible person with self-only HSA-qualified coverage

Family coverage

$8,750

Maximum annual contribution for eligible family HSA-qualified coverage

Age 55+ catch-up contribution

$1,000

Additional contribution for eligible account holders age 55 or older

Self-only coverage with catch-up

$5,400

$4,400 annual limit plus the $1,000 catch-up contribution

Family coverage with one catch-up

$9,750

$8,750 family limit plus one eligible spouse catch-up

Family coverage with two spouse catch-ups

$10,750

$8,750 family limit plus two separate $1,000 catch-up contributions

The family limit is shared. The catch-up contribution is personal. If both spouses are 55 or older and both are eligible, each spouse needs a separate HSA for that spouse catch-up contribution.

This detail causes confusion because families sometimes assume the entire $10,750 can go into one account. The shared family contribution can be split between spouses, but each $1,000 catch-up belongs in an HSA under the name of the spouse making that catch-up contribution.

2026 HSA Limits Compared With 2025

The 2026 limit is higher than the 2025 limit, while the catch-up contribution remains unchanged. The high-deductible health plan thresholds also moved higher.

| Limit Or HDHP Rule | 2025 | 2026 | Change |

| Self-only HSA contribution limit | $4,300 | $4,400 | +$100 |

| Family HSA contribution limit | $8,550 | $8,750 | +$200 |

| Age 55+ catch-up contribution | $1,000 | $1,000 | No change |

| Self-only HDHP minimum deductible | $1,650 | $1,700 | +$50 |

| Family HDHP minimum deductible | $3,300 | $3,400 | +$100 |

| Self-only HDHP maximum out-of-pocket limit | $8,300 | $8,500 | +$200 |

| Family HDHP maximum out-of-pocket limit | $16,600 | $17,000 | +$400 |

The increase gives households slightly more tax-advantaged room for medical costs, but the higher deductible and out-of-pocket figures show the tradeoff. HSAs can help with taxes and savings, yet they are tied to plans that require more upfront cost sharing before the plan pays more of the bill.

What Counts As An HSA-Eligible Health Plan In 2026

View this post on Instagram

To contribute to an HSA, a person generally needs HSA-qualified high-deductible health plan coverage, often called an HDHP, and no disqualifying other coverage.

For 2026, the IRS defines a qualifying HDHP as a plan with a deductible of at least $1,700 for self-only coverage or $3,400 for family coverage. The plan also must keep annual out-of-pocket expenses, excluding premiums, at no more than $8,500 for self-only coverage or $17,000 for family coverage.

| 2026 HDHP Requirement | Self-Only Coverage | Family Coverage |

| Minimum annual deductible | $1,700 | $3,400 |

| Maximum annual out-of-pocket expenses | $8,500 | $17,000 |

| HSA contribution limit | $4,400 | $8,750 |

| Age 55+ catch-up contribution | +$1,000 | +$1,000 per eligible spouse, through separate HSAs |

Out-of-pocket expenses include deductibles, copayments and other covered cost sharing. Premiums are not counted for this limit. That distinction is important because a lower-premium plan can still expose a household to a high deductible and large medical bills during the year.

Health plan labels also need careful reading. A plan with a high deductible is not automatically HSA-qualified. The plan must satisfy the federal HSA rules, or fall under one of the 2026 compatibility changes described below.

We previously covered more about the U.S. healthcare spending by state in 2026, where healthcare costs vary widely by state and remain a major budget concern for households.

The 2026 Rule Change That Expands HSA Access

The biggest 2026 HSA development is not the $100 or $200 increase in contribution room. The wider change is eligibility.

The IRS guidance on new HSA tax benefits says certain Bronze and Catastrophic plans are treated as HSA-compatible beginning January 1, 2026. The guidance also addresses telehealth and direct primary care arrangements.

HealthCare.gov explains the consumer-facing result: more 2026 Marketplace plans, including Bronze and Catastrophic plans, can work with Health Savings Accounts.

| 2026 HSA Change | What Changed | Why It Affects Account Holders |

| Bronze and Catastrophic plans | Certain plans are treated as HSA-compatible | People using lower-premium individual coverage may have more HSA options |

| Telehealth relief | HSA-compatible plans can cover certain remote care before the deductible | Telehealth access does not automatically ruin HSA eligibility when the rules are met |

| Direct primary care arrangements | Certain arrangements no longer automatically block HSA eligibility | People using membership-based primary care get clearer HSA treatment |

| Tax-free HSA use for some DPC fees | Eligible direct primary care fees can be paid with HSA funds | Account holders may have another medical use for tax-free HSA dollars |

The change is especially relevant for self-employed people, contractors, early retirees before Medicare and households buying individual coverage. It expands access, but it does not remove the contribution caps or the other eligibility rules.

Who Can Contribute To HSA In 2026?

A person generally needs to meet all of these conditions to contribute to an HSA in 2026:

- Have HSA-compatible health coverage

- Have no disqualifying non-HDHP coverage

- Not be enrolled in Medicare

- Not be claimed as a dependent on another taxpayer return

- Stay within the annual IRS contribution limit

Employer coverage, Marketplace coverage and self-employed coverage can all qualify if the plan meets the HSA rules. The safest step is to confirm HSA compatibility through the employer benefits office, insurer, Marketplace listing, HSA provider or plan documents before making contributions.

Eligibility is usually measured by month. A person who is eligible for only part of the year may have to prorate the contribution limit unless the last-month rule applies.

Employer Contributions Count Toward The HSA Limit

Employer contributions can be valuable, but they reduce the amount the employee can add. They are part of the same annual IRS limit.

| Example | 2026 HSA Limit | Employer Contribution | Maximum Employee Contribution |

| Self-only coverage, under age 55 | $4,400 | $1,000 | $3,400 |

| Self-only coverage, age 55+ | $5,400 | $1,000 | $4,400 |

| Family coverage, under age 55 | $8,750 | $1,500 | $7,250 |

| Family coverage, one eligible catch-up | $9,750 | $1,500 | $8,250 |

This is one of the most common HSA mistakes. People track only payroll deductions and forget employer deposits. Wellness incentives, seed money and employer-funded deposits can create an excess contribution if the employee does not subtract them from the annual cap.

Catch-Up Contributions For Married Couples

The HSA catch-up rule works differently from the main family limit. The family limit is shared, but the catch-up is tied to the individual account holder.

| Married Couple Scenario | Maximum 2026 HSA Amount | How It Works |

| Family coverage, both spouses under age 55 | $8,750 | The family limit is shared between spouses |

| Family coverage, one spouse age 55+ | $9,750 | The household can use the $8,750 family limit plus one $1,000 catch-up |

| Family coverage, both spouses age 55+ | $10,750 | The household can use the $8,750 family limit plus two separate $1,000 catch-ups |

If both spouses are 55 or older, each spouse needs a separate HSA for that spouse own $1,000 catch-up. One spouse cannot place both catch-up contributions into a single HSA.

This rule is easy to miss because a couple may use one family health plan and one main HSA for most expenses. The catch-up contribution still follows the individual account rule.

Medicare And HSAs – The Rule That Catches People Off Guard

Medicare enrollment generally stops new HSA contributions. Existing HSA funds remain available, but the account holder can no longer contribute after Medicare enrollment begins.

This is especially important for people approaching age 65. Medicare Part A can be retroactive in some situations. A person who delays Medicare while working and then enrolls later may need to stop HSA contributions before the enrollment date shown on Medicare records.

| Medicare Situation | HSA Contribution Result |

| Not enrolled in Medicare and otherwise HSA-eligible | Contributions can continue within the annual limit |

| Enrolled in Medicare Part A or Part B | New HSA contributions generally must stop |

| Existing HSA balance after Medicare starts | Funds can still be used for qualified medical expenses |

| Medicare enrollment with retroactive Part A | Contribution timing needs review to avoid excess contributions |

Workers who plan to keep employer coverage after age 65 should check Medicare timing before continuing payroll HSA deductions. This is one of the areas where a payroll setting can create a tax problem without the account holder noticing immediately.

2026 HSA Contribution Deadline

HSA contributions for a tax year can generally be made until the federal tax filing deadline for that year. For 2026 contributions, the deadline generally falls in April 2027 for most taxpayers.

The contribution must be coded for the correct tax year by the HSA provider. A deposit made in early 2027 can be applied to 2026 or 2027, depending on how the account holder submits it.

| Contribution Timing | How To Treat It |

| Payroll deduction during 2026 | Usually treated as a 2026 contribution |

| Direct contribution during 2026 | Usually treated as a 2026 contribution |

| Direct contribution in early 2027 before the filing deadline | Can usually be applied to 2026 if the account holder selects 2026 |

| Contribution submitted with the wrong tax year selected | May need custodian correction |

This is a practical issue at tax time. Someone who wants to top off a 2026 HSA in early 2027 should confirm the deposit year before submitting the contribution.

What Happens If You Contribute Too Much?

Excess HSA contributions can create tax penalties. If a person contributes above the allowed limit, the excess amount can face a 6% excise tax for each year it remains in the account.

The usual fix is to contact the HSA provider and remove the excess contribution, plus any related earnings, before the tax filing deadline. Earnings tied to the excess contribution may be taxable.

- Employer contributions were not counted

- Family coverage changed to self-only coverage during the year

- HSA eligibility started or ended midyear

- Medicare enrollment began while payroll deductions continued

- Both spouses treated the family limit as separate limits

- A prior-year contribution was submitted for the wrong tax year

- The last-month rule was used, but the testing period failed

The best way to avoid excess contributions is to check deposits during the year, not only during tax preparation.

How The Last-Month Rule Works?

The last-month rule can allow a person who is HSA-eligible on December 1 to contribute the full-year amount, even if that person was not eligible for every month of the year.

The rule can help people who gain HSA-compatible coverage late in the year. The risk is the testing period. The account holder generally needs to stay eligible through the end of the following year. If eligibility ends too soon, part of the contribution can become taxable and may face an additional penalty.

| Situation | Possible Contribution Result | Risk |

| Eligible for all 12 months | Full annual contribution limit generally applies | Low, if no disqualifying coverage exists |

| Eligible for only part of the year | Contribution may need monthly proration | Overfunding risk |

| Eligible on December 1 | Last-month rule may allow full-year contribution | Testing period must be met |

| Uses last-month rule and loses eligibility the following year | Extra contribution may become taxable and may face penalty | High if coverage change is likely |

The last-month rule is useful for stable coverage situations. It is less useful when the account holder expects a job change, plan change, Medicare enrollment or a move to non-HDHP coverage.

Why HSAs Remain Useful?

HSAs have a tax structure that few accounts can match. Contributions can reduce taxable income. Growth inside the account can be tax-free. Withdrawals for qualified medical expenses can also be tax-free.

| HSA Feature | How It Helps |

| Tax-advantaged contributions | Payroll contributions are usually pre-tax, while direct contributions may be deductible |

| Tax-free growth | Interest and investment gains can grow without current tax |

| Tax-free qualified withdrawals | Funds used for qualified medical expenses are not taxed |

| No use-it-or-lose-it rule | Unused HSA money can roll over year after year |

| Portability | The account belongs to the account holder after job changes or plan changes |

| Investment option at many providers | Balances can be invested if the provider allows and the account holder has enough cash reserve |

The tax benefits are meaningful, but the account works best when the household can handle the deductible and out-of-pocket exposure tied to the health plan. A person with thin cash reserves may need to balance HSA deposits with emergency savings.

Our team at NCH Stats has covered related household pressure in its report on healthcare costs in the U.S., including how medical expenses vary by state and household situation.

How HSA Accounts Are Being Used?

HSAs have grown into a large part of the U.S. benefits system. Devenir reported that HSAs held nearly $174 billion across 41.7 million accounts at year-end 2025. Total HSA assets rose 19% year over year.

The same report showed that investment assets reached nearly $85 billion, while about 4.2 million accounts, or about 10% of all HSAs, held invested dollars.

| HSA Market Measure | Latest Devenir Figure | What It Shows |

| Total HSA assets | Nearly $174 billion at year-end 2025 | HSAs are a major healthcare savings tool |

| Total HSA accounts | 41.7 million | Account use continues to grow |

| Investment assets | Nearly $85 billion | More account holders are using HSAs for long-term growth |

| Accounts with invested dollars | About 4.2 million, or about 10% of all HSAs | Most accounts are still used mainly for cash spending |

| Contributions during 2025 | Nearly $60 billion | Large inflows continue through payroll and direct deposits |

| Withdrawals during 2025 | Nearly $45 billion | Many users spend HSA funds on current medical bills |

These figures show two different HSA users. One group spends HSA money quickly on current medical costs. Another group invests part of the balance and treats the account as a long-term healthcare reserve. Both approaches are valid, but they lead to very different account balances over time.

Policy Tradeoffs Around HSAs

HSAs help many account holders, but they also raise policy questions. The Congressional Research Service report on Health Savings Accounts reviews HSA eligibility, qualified HDHP rules, contributions, withdrawals, tax treatment and broader policy issues.

A Government Accountability Office report also described HSAs as tax-advantaged accounts tied to HSA-eligible HDHPs and noted that HSA-related tax benefits carry federal revenue costs. GAO reported that Treasury estimated HSA-related tax-advantaged contributions and withdrawals cost nearly $13 billion in forgone federal income tax revenue in 2023.

The policy tradeoff is direct. HSAs can help people save and pay medical bills with tax benefits. The largest long-term benefits usually go to people who can afford to contribute, avoid immediate withdrawals and invest part of the balance. People with tighter budgets may still benefit, but they may use the account mainly for current bills.

How Much To Contribute In 2026?

View this post on Instagram

The maximum contribution is not automatically the right contribution for every household. The right amount depends on medical needs, plan deductible, employer deposits, household cash flow, debt and emergency savings.

| Household Situation | Possible HSA Strategy |

| Employer offers HSA money | Contribute enough to receive the employer deposit if employee action is required |

| Recurring prescriptions or appointments | Fund enough for predictable medical costs |

| High deductible with limited savings | Build cash reserves along with HSA contributions |

| Healthy household with stable income | Consider contributing above expected spending and saving the rest |

| Age 55 or older and eligible | Use the $1,000 catch-up if the budget allows |

| Medicare enrollment is near | Check the final eligible contribution month before making deposits |

People who cannot max out an HSA can still benefit. Smaller payroll deposits can cover prescriptions, dental care, vision care, deductibles and urgent bills with tax-advantaged money.

Qualified Medical Expenses

HSA funds can be used tax-free for qualified medical expenses. The IRS explains qualified medical expenses in Publication 969 and through rules tied to medical expense deductions.

| Common HSA-Qualified Expense | Common Expense That Usually Needs Caution |

| Deductibles | Most health insurance premiums |

| Copayments and coinsurance | Cosmetic procedures without medical need |

| Prescription drugs | General wellness products without a qualifying medical purpose |

| Dental care | Expenses already reimbursed by insurance |

| Vision care | Non-medical personal care items |

| Many over-the-counter medicines | Items not recognized as qualified medical expenses |

| Certain direct primary care fees under 2026 rules | Fees outside the allowed DPC rules |

Account holders should keep receipts and records. HSA providers may issue tax forms, but the taxpayer remains responsible for proving that withdrawals were used for qualified medical expenses.

HSA, FSA And HRA Differences

HSAs are often confused with Flexible Spending Accounts and Health Reimbursement Arrangements. The differences matter because the accounts have different ownership, rollover and eligibility rules.

| Account Type | Who Owns It | Rollover Treatment | Main Use |

| HSA | Individual account holder | Unused funds roll over year after year | Tax-advantaged medical savings tied to HSA-compatible coverage |

| Health FSA | Employer plan | Use-it-or-lose-it rules usually apply, with limited carryover or grace period options | Short-term medical spending through an employer plan |

| HRA | Employer arrangement | Rules depend on plan design | Employer-funded reimbursement for eligible medical costs |

An HSA is portable. If the account holder changes jobs, leaves the employer or changes health plans, the HSA balance stays with that person. Contributions may stop if eligibility ends, but existing funds remain available for qualified medical expenses.

Common Mistakes to Avoid

Most HSA errors come from timing, coverage changes or misunderstanding the family limit.

| Mistake | Why It Creates A Problem | How To Avoid It |

| Contributing after Medicare enrollment | Medicare enrollment generally ends HSA contribution eligibility | Stop contributions before Medicare eligibility blocks them |

| Ignoring employer deposits | Employer money counts toward the same annual limit | Subtract employer contributions before setting payroll deductions |

| Assuming spouses get two family limits | The family limit is shared | Coordinate spouse contributions during the year |

| Putting both catch-up contributions in one HSA | Each spouse catch-up needs a separate HSA | Open separate HSAs for age-55 catch-ups |

| Using the last-month rule without planning | Failing the testing period can create tax and penalty issues | Use the rule only when coverage is expected to remain stable |

| Choosing the wrong tax year for a contribution | A prior-year top-off may be applied to the wrong year | Confirm the contribution year with the HSA provider |

These mistakes are preventable. A midyear contribution check is often enough to catch problems before tax filing.

Practical Examples

The following examples show how the limit works in common situations.

| Example | Coverage And Age | 2026 Maximum | Reason |

| Single employee | Self-only HDHP, age 38 | $4,400 | Self-only limit applies |

| Single employee age 57 | Self-only HDHP, age 57 | $5,400 | Self-only limit plus $1,000 catch-up |

| Married couple with children | Family HDHP, both under 55 | $8,750 | Family limit applies |

| Married couple, one spouse age 56 | Family HDHP, one eligible catch-up | $9,750 | Family limit plus one catch-up |

| Married couple, both age 56 | Family HDHP, both eligible | $10,750 | Family limit plus two separate catch-ups |

| Worker with employer deposit | Self-only HDHP, employer adds $750 | $3,650 employee contribution under age 55 | $4,400 limit minus employer deposit |

These examples assume the person is eligible for the full year. Midyear eligibility changes can lower the permitted contribution unless the last-month rule applies.

How Can HSAs Fit Into A Household Budget?

An HSA can support three different goals: current medical spending, emergency protection and long-term healthcare savings. The right balance depends on the household.

A person with ongoing medical costs may use the HSA mainly for current bills. A person with fewer medical costs may save receipts, pay smaller bills from regular cash flow and let the HSA balance grow. A family with limited savings may use the HSA as a dedicated medical reserve and keep the balance in cash.

| HSA Use | Best Fit | Tradeoff |

| Spend as bills arrive | Households with recurring care or tight cash flow | Less long-term growth |

| Keep a cash reserve | Households with high deductible exposure | Lower investment return |

| Invest part of the HSA | Households able to pay some medical bills from other funds | Investment risk and need for cash planning |

| Save receipts for later reimbursement | Organized account holders with enough cash flow | Requires careful recordkeeping |

The account is flexible, but that flexibility requires discipline. HSA users should know the deductible, keep receipts, track contributions and avoid withdrawals for nonqualified expenses.

What Happens After Age 65?

After age 65, HSA funds can still be used tax-free for qualified medical expenses. HSA funds used for nonmedical expenses after age 65 are generally taxable as income, but they are not subject to the additional penalty that applies before age 65.

This feature makes HSAs useful for retirement healthcare planning. The account can help pay for qualified medical expenses, and it can provide taxable backup funds after 65 if needed.

However, Medicare enrollment still blocks new HSA contributions. A person can spend an existing HSA after Medicare starts, but generally cannot keep adding money.

What To Check Before Setting Contributions?

Before setting payroll deductions or making direct HSA deposits, account holders should check the following:

- Confirm the health plan is HSA-compatible

- Check whether employer deposits are being made

- Confirm whether coverage is self-only or family

- Check spouse contributions if married

- Check whether either spouse is eligible for the age-55 catch-up

- Review Medicare timing for anyone near age 65

- Estimate deductible exposure and expected medical bills

- Leave enough cash for nonmedical emergencies

- Track the contribution year for direct deposits

This checklist is simple, but it prevents most HSA tax mistakes.

Methodology And Sources

This article uses IRS Revenue Procedure 2025-19 as the primary source for 2026 HSA contribution limits and HDHP thresholds. It uses IRS guidance on 2026 HSA tax benefits and HealthCare.gov HSA guidance for Bronze, Catastrophic, telehealth and direct primary care rule changes.

Consumer-facing contribution explanations were checked against Fidelity and Empower. Policy context comes from the Congressional Research Service HSA report and the Government Accountability Office HSA report. Market data comes from Devenir 2025 year-end HSA research.

Bottom Line

The 2026 HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage. Eligible account holders age 55 or older can add a $1,000 catch-up contribution.

Those numbers are only the starting point. The plan must be HSA-compatible, employer contributions count toward the limit, Medicare generally stops new contributions, and married couples need to handle catch-up contributions carefully.

The 2026 rules also expand HSA access for certain Bronze and Catastrophic plans and clarify treatment for telehealth and direct primary care. For households facing higher medical costs, the HSA remains a useful tax-advantaged tool, but it works best when contribution limits, plan rules and household cash flow are managed together.