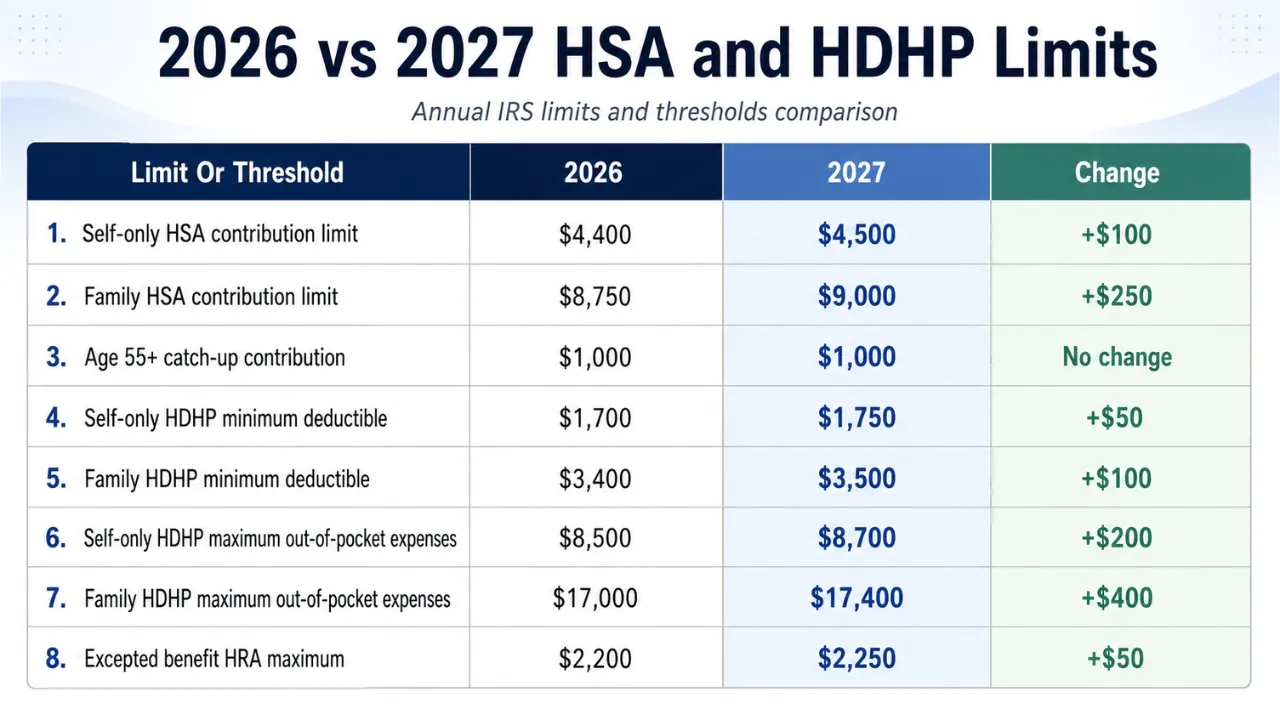

The maximum HSA contribution for 2027 is $4,500 for self-only coverage and $9,000 for family coverage, according to IRS Revenue Procedure 2026-24.

Eligible account holders who are 55 or older can add a $1,000 catch-up contribution. That brings the 2027 maximum to $5,500 for self-only coverage with catch-up, $10,000 for family coverage with one eligible catch-up, and $11,000 for family coverage when both spouses qualify and each uses a separate HSA for the catch-up amount.

Out team at NCH Stats has covered the broader cost picture in its report on U.S. healthcare spending by state, and the same pressure explains why HSA limits matter for workers, families, self-employed people and anyone choosing a high-deductible plan.

What is the Maximum HSA Contribution for 2027?

Coverage Or Situation

Maximum 2027 HSA Contribution

How The Limit Works

Self-only coverage

$4,500

Maximum annual HSA contribution for eligible self-only coverage

Family coverage

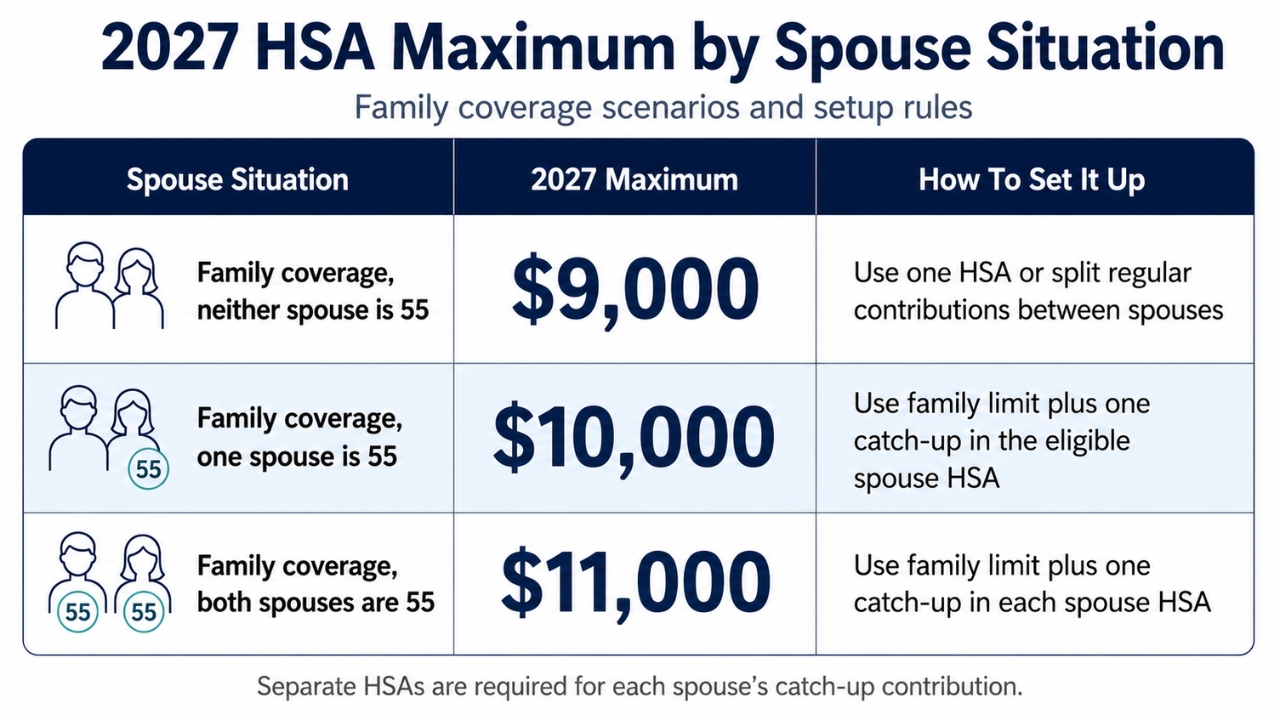

$9,000

Maximum annual HSA contribution for eligible family coverage

Age 55+ catch-up

$1,000

Additional contribution for an eligible account holder age 55 or older

Self-only coverage with catch-up

$5,500

$4,500 self-only limit plus $1,000 catch-up

Family coverage with one catch-up

$10,000

$9,000 family limit plus one $1,000 catch-up

Family coverage with two spouse catch-ups

$11,000

$9,000 family limit plus two separate $1,000 catch-ups

The contribution cap includes money from every source. Employee payroll deductions, direct deposits, employer seed money, employer wellness incentives and third-party deposits all count toward the same IRS annual limit.

The catch-up contribution is tied to the individual account holder. A married couple with family coverage shares the $9,000 family limit. If both spouses are 55 or older and both remain HSA-eligible, each spouse can add $1,000, but each catch-up must go into an HSA in that spouse’s name.

Changes Compared to the Previous Year

The 2027 HSA limits are higher than the 2026 limits, and the plan-design thresholds rose as well. The increase affects payroll elections, employer plan design, open enrollment, Marketplace plan choices and tax planning.

The contribution increase gives eligible households more room to set aside tax-advantaged money. The deductible and out-of-pocket increases show the other side of HSA planning: these accounts are tied to plans that can require higher cost-sharing when care is needed.

2027 HDHP Rules Behind HSA Eligibility

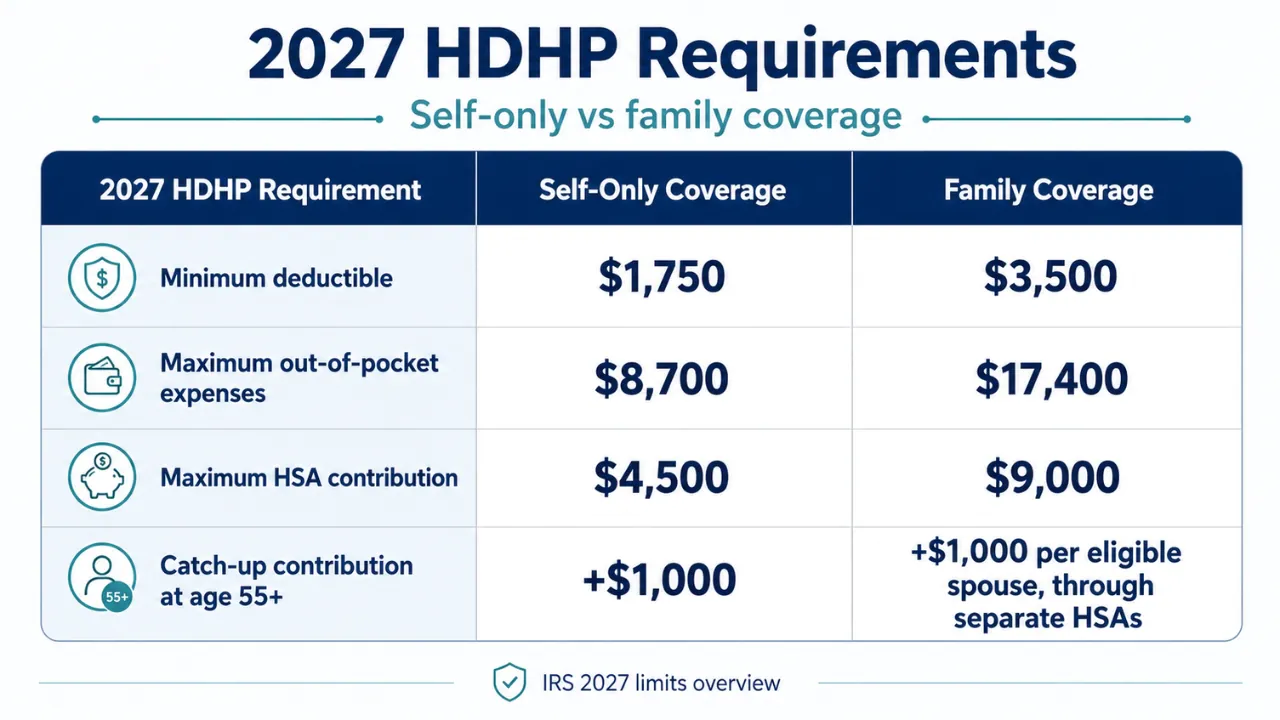

An HSA contribution requires eligible coverage. The account alone is not enough. A person generally needs a qualifying high-deductible health plan, no disqualifying other coverage, no Medicare enrollment, and no dependent status on another taxpayer return.

For 2027, the IRS defines a qualifying high-deductible health plan as one with a deductible of at least $1,750 for self-only coverage or $3,500 for family coverage. The plan also must keep annual out-of-pocket expenses, excluding premiums, below the IRS ceiling.

The out-of-pocket ceiling includes deductibles, copayments, and other covered cost-sharing. It does not include premiums. That means a lower monthly premium can still come with a larger bill when a surgery, hospitalization, specialist visit, or expensive prescription appears.

This is where the HSA limit connects with everyday medical spending. NCH Stats has also covered healthcare costs in the U.S., including how patient costs vary by state and why out-of-pocket expenses matter for insured households.

HSA Eligibility Is Broader Than It Used To Be

Recent federal changes make the 2027 HSA conversation different from older HSA planning. The limit increase is only one part of the story. The bigger planning issue is who can use the account.

The IRS guidance on new HSA tax benefits explains that certain Bronze and Catastrophic plans are treated as HSA-compatible. The IRS also addressed permanent telehealth relief and direct primary care arrangements.

HealthCare.gov says more Marketplace plans, including Bronze and Catastrophic plans, can work with Health Savings Accounts.

Rule Area

2027 Planning Impact

Who Should Pay Attention

Bronze plans

More Bronze coverage can pair with HSAs

Marketplace shoppers, self-employed workers, contractors and early retirees before Medicare

Catastrophic plans

More Catastrophic coverage can pair with HSAs

People eligible for Catastrophic coverage who want lower premiums and HSA access

Telehealth

Pre-deductible telehealth relief is permanent when requirements are met

Employers, workers and plan sponsors using remote care

Direct primary care

Certain arrangements no longer automatically block HSA eligibility

Patients using membership-based primary care

DPC fee thresholds

IRS Rev. Proc. 2026-24 keeps monthly aggregate DPCSA limits at $150 for one person and $300 for more than one person for 2027

Families combining direct primary care with HSA-compatible coverage

How To Calculate HSA Contribution Limit?

View this post on Instagram

The cleanest way to avoid HSA mistakes is to calculate the limit in order. Start with coverage type. Add catch-up eligibility. Subtract employer deposits. Then adjust for partial-year eligibility, Medicare, or coverage changes.

Step

Question To Ask

Why It Changes The Contribution

1

Is coverage self-only or family?

This decides whether the base limit is $4,500 or $9,000

2

Was the person HSA-eligible for the full year?

Partial-year eligibility may require proration

3

Is the account holder age 55 or older by the end of 2027?

The $1,000 catch-up may apply

4

Did an employer or another person contribute?

Those deposits count toward the same cap

5

Did Medicare enrollment begin?

Medicare generally stops new HSA contributions

6

Did family status or plan coverage change?

Switching coverage can change the allowed contribution

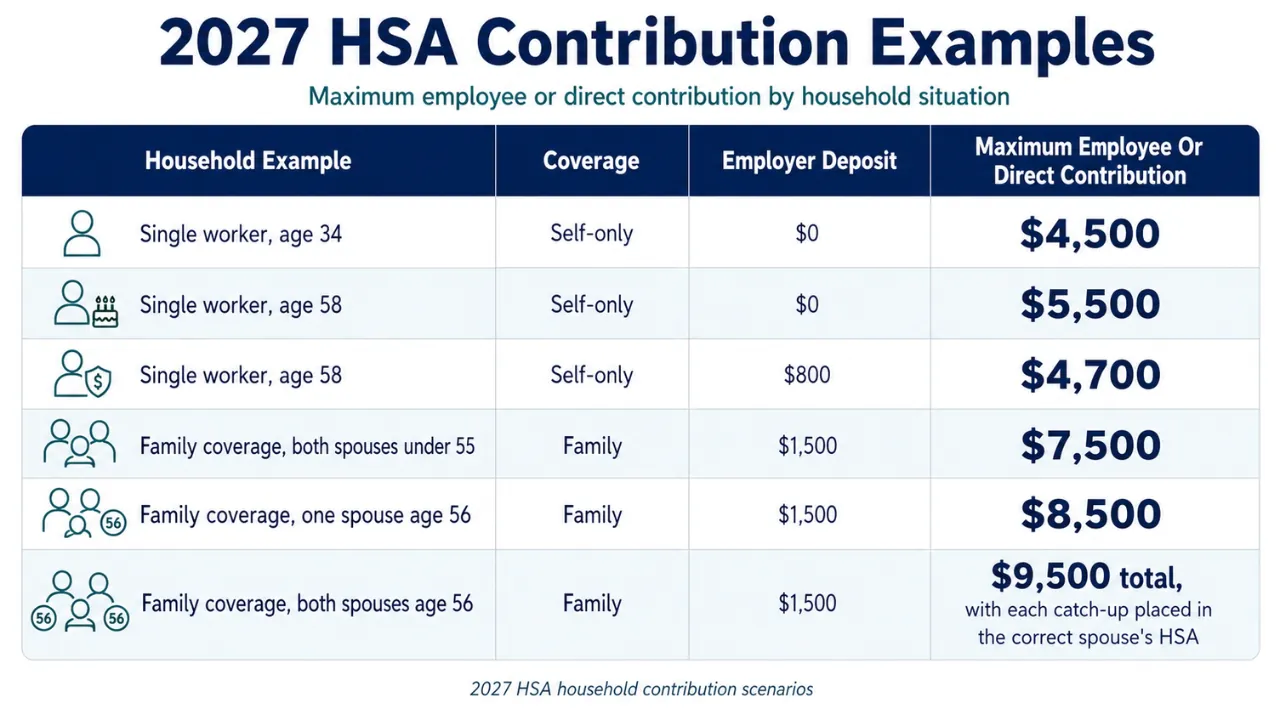

Contribution Examples

The following examples show how the 2027 maximum works in normal household situations. These examples assume full-year eligibility unless the description says otherwise.

Open Enrollment

The HSA limit matters after the household decides whether the plan itself fits.

Open Enrollment Question

Why It Belongs In The 2027 HSA Decision

How much is the monthly premium?

A lower premium can free cash for HSA contributions, but may come with higher cost sharing

What is the deductible?

The household may need to pay this amount before the plan covers more care

What is the out-of-pocket maximum?

This shows the worst-case in-network cost exposure, excluding premiums

Does the employer contribute to the HSA?

Employer money can make the HSA plan more attractive

Are expected prescriptions covered well?

Drug costs can change the true value of the plan

Can the household cover the deductible if care happens early in the year?

An HSA helps, but cash timing still counts

Hospital bills are one reason this calculation matters. We already explained how even insured patients can face high out-of-pocket exposure in a report about the average cost of a hospital stay in the U.S.

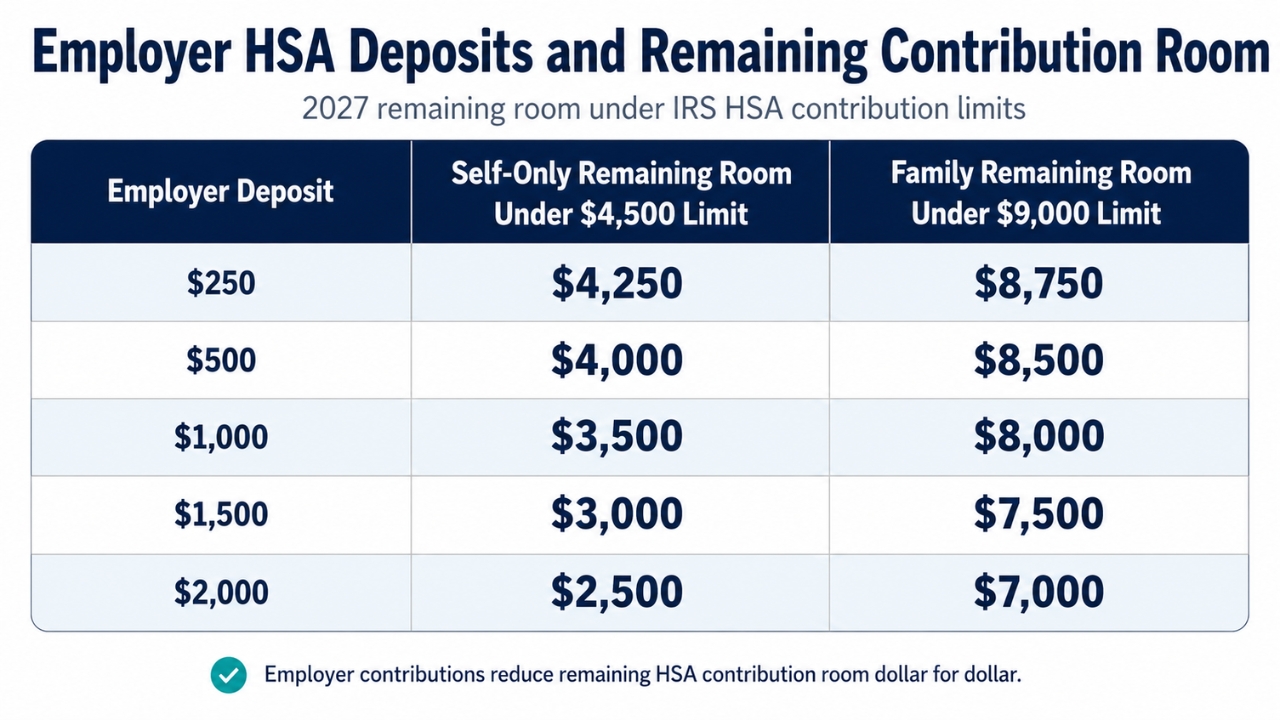

How Employer Contributions Change The Decision?

Employer HSA deposits can make a high-deductible plan more practical. They reduce the amount an employee needs to contribute from personal cash, but they also reduce the remaining room under the IRS limit.

Spouses And The $11,000 Maximum

The highest common 2027 HSA number is $11,000, but that figure only applies in a specific case: family coverage, both spouses eligible, both age 55 or older, and both catch-up contributions handled through separate HSAs.

Medicare Timing Can Reduce The 2027 Limit

Medicare enrollment generally ends the ability to make new HSA contributions. Existing HSA funds remain available for qualified medical expenses, but new deposits usually stop once Medicare coverage begins.

Medicare Situation

HSA Contribution Result

Practical Step

No Medicare enrollment and otherwise eligible

Contributions can continue

Use the normal 2027 limit calculation

Medicare starts in 2027

The contribution limit may need proration

Stop payroll deductions before the ineligible period

Medicare Part A applies retroactively

Prior contributions may need review

Check the Medicare effective date

Existing HSA after Medicare starts

Funds can still be used

Keep receipts for qualified medical expenses

Partial-Year Eligibility And The Last-Month Rule

When employees maximize their HSA contributions, they maximize the benefits. Starting in 2027, they can contribute $4,500 to your HSA for single coverage or $9,000 for family coverage! pic.twitter.com/h3IqT3uGCb

— HSA Bank (@hsabank) June 9, 2026

A person who is HSA-eligible for only part of 2027 may have a smaller contribution limit. The monthly limit is generally based on the number of eligible months.

The last-month rule can change that. A person who is HSA-eligible on December 1, 2027, may be allowed to contribute the full-year amount. The tradeoff is a testing period that generally requires continued eligibility through the end of the following year.

Coverage Timing

Possible Contribution Treatment

Main Risk

Eligible for all 12 months

Full annual limit generally applies

Low if no disqualifying coverage exists

Eligible for fewer than 12 months

Monthly proration may apply

Overfunding if the full limit is used without qualifying for the last-month rule

Eligible on December 1, 2027

Last-month rule may allow full annual limit

The testing period must be met

Loses eligibility during the testing period

An extra amount may become taxable and may face a penalty

Job changes, plan changes, or Medicare can create problems

2027 Contribution Deadline

HSA contributions for 2027 can generally be made until the federal tax filing deadline for the 2027 tax year. For most taxpayers, that means April 2028.

When The Deposit Is Made

Possible Tax Year Treatment

What To Check

Payroll contribution during 2027

Usually 2027

Check year-to-date payroll totals

Direct contribution during 2027

Usually 2027

Confirm account posting

Direct contribution before the filing deadline in 2028

Can usually be coded to 2027

Select the correct year before submitting

Deposit coded to the wrong year

May need correction

Contact the HSA custodian quickly

HSA Market Data Shows Two Different Account Users

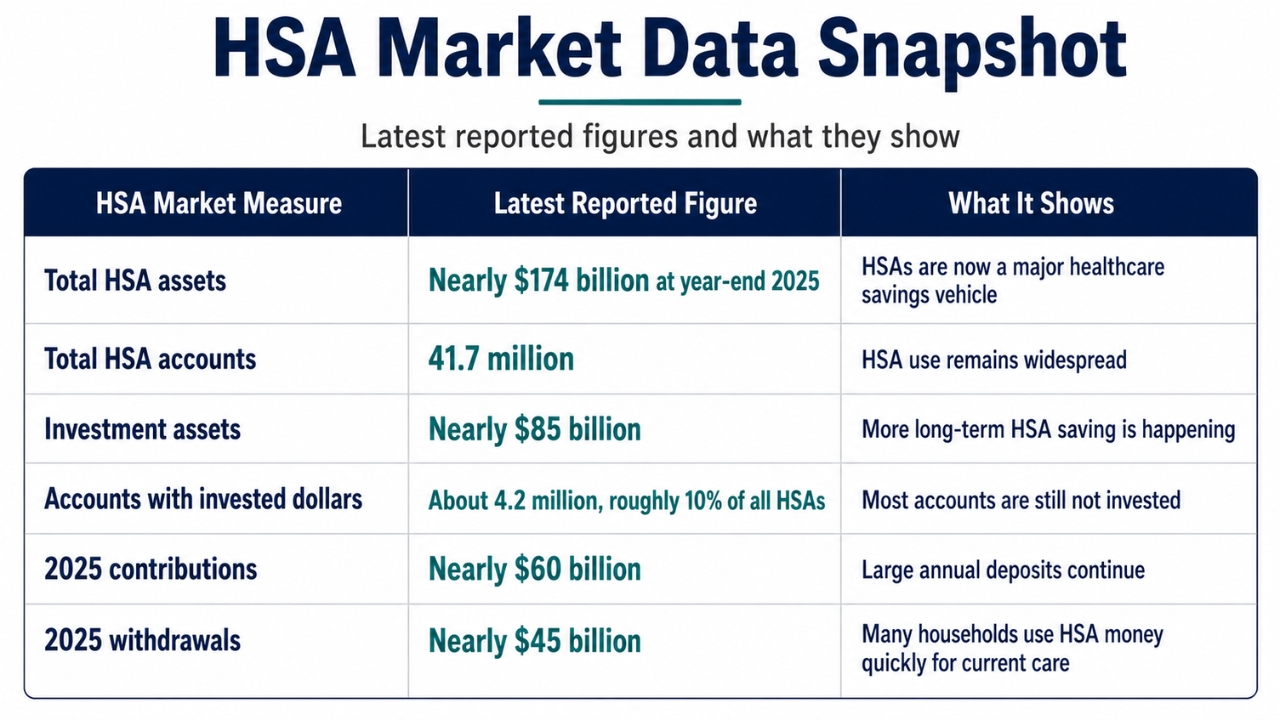

HSA planning looks different because account holders use HSAs in two very different ways. Some use the account for current bills. Others save and invest part of the balance for future healthcare costs.

Devenir reported that HSAs held nearly $174 billion in assets across 41.7 million accounts at year-end 2025. Assets rose 19% year over year. Investment assets reached nearly $85 billion, up 33%.

The Limit Is Useful But Uneven

HSAs have a rare tax structure. Contributions can reduce taxable income. Growth inside the account can avoid tax. Withdrawals for qualified medical expenses can also avoid tax.

The benefit is larger for people who can afford to contribute and leave money in the account. Households with tight monthly budgets may still benefit, but many use the HSA mostly as a pass-through account for current care.

A Government Accountability Office report described that policy concern. GAO noted that HSAs can earn interest, be invested, and be carried into retirement, while policymakers have questioned whether higher-income people gain more because they have more ability to save.

The uninsured and underinsured backdrop also matters. NCH Stats has tracked long-term coverage gaps in its report on the U.S. uninsured rate by year, and those gaps help explain why tax-advantaged medical savings remain part of the policy debate.

What Counts As A Qualified Medical Expense?

HSA funds can be used tax-free for qualified medical expenses. IRS Publication 969 explains the general HSA tax rules and account treatment.

Common HSA-Qualified Expense

Expense That Needs Caution

Deductibles

Most health insurance premiums

Copayments and coinsurance

Cosmetic care without medical need

Prescription drugs

Items reimbursed by another plan

Dental care

General wellness items without a medical purpose

Vision care

Nonmedical personal care products

Many over-the-counter medicines

Expenses outside the IRS qualified medical rules

Certain direct primary care fees are under federal rules

DPC fees above the allowed limits or outside the rules

How To Use The 2027 Limit Without Overfunding?

Many HSA errors can be avoided with a simple midyear check. The account holder should compare the IRS cap, employer deposits, payroll deductions already made, planned deposits, catch-up eligibility, and coverage changes.

Potential Mistake

Why It Happens

How To Avoid It

Ignoring employer contributions

Payroll deposits are tracked, but the employer’s seed money is forgotten

Subtract employer deposits from the annual cap

Continuing after Medicare starts

Payroll deductions keep running after eligibility ends

Stop contributions before Medicare blocks new deposits

Using two family limits

Spouses each assume family coverage gives them a full cap

Remember that the family limit is shared

Putting both catch-ups in one account

Both spouses use the same HSA

Each eligible spouse needs a separate HSA for catch-up

Missing partial-year rules

Coverage starts or ends midyear

Prorate unless the last-month rule applies and the testing period is met

Wrong contribution year

Early-year deposit is coded incorrectly

Confirm the tax year with the custodian

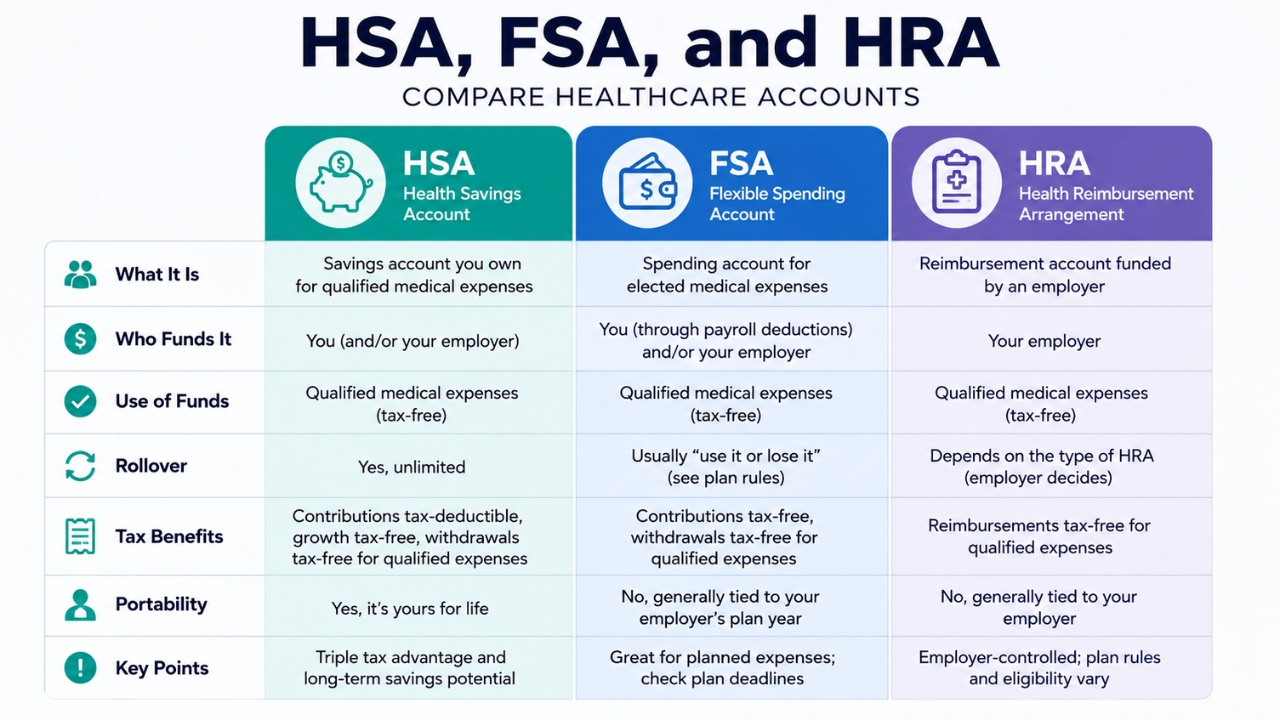

HSA, FSA, and HRA – Differences For the Next Year

HSAs are often confused with flexible spending accounts and health reimbursement arrangements. They are not the same account.

Account Type

Who Controls It

Rollover Treatment

Main Planning Use

HSA

Individual account holder

Unused funds roll over year after year

Medical savings tied to HSA-compatible coverage

Health FSA

Employer plan

Use-it-or-lose-it rules usually apply, with limited carryover or grace-period options

Short-term medical spending through an employer benefit

HRA

Employer arrangement

Depends on employer plan design

Employer-funded medical reimbursement

Excepted benefit HRA

Employer arrangement

Depends on plan design

Limited benefits, with a 2027 maximum of $2,250

What Employers Should Update For 2027?

Employers and benefits teams need the 2027 figures for plan documents, payroll systems, open enrollment materials, and employee education.

The maximum is not automatically the right amount. The right contribution depends on medical costs, cash flow, debt, employer deposits, and how much risk the household can handle. This article uses IRS Revenue Procedure 2026-24 as the primary source for 2027 HSA contribution limits, HDHP minimum deductibles, HDHP maximum out-of-pocket amounts, direct primary care monthly fee thresholds, and the excepted benefit HRA amount. Plan-eligibility changes are based on IRS guidance on new HSA tax benefits and HealthCare.gov HSA plan information. General HSA tax rules and qualified medical expense treatment are based on IRS Publication 969. Policy background comes from the Congressional Research Service report on Health Savings Accounts and the Government Accountability Office report on HSA features and use. Market data comes from the Devenir 2025 year-end HSA research report. The maximum HSA contribution for 2027 is $4,500 for self-only coverage and $9,000 for family coverage. Eligible account holders age 55 or older can add $1,000. The largest regular household figure is $11,000, but only for family coverage when both spouses are eligible, both are at least 55, and both use separate HSAs for catch-up contributions. The 2027 limit is about more than a higher IRS number. It affects how households plan around HSA-compatible coverage, employer deposits, Medicare timing, spouse rules, Marketplace plan changes, and rising healthcare costs. Used carefully, an HSA can help with current medical bills and future healthcare savings. Used without tracking the rules, it can create avoidable tax problems.

How Much Should A Household Put In For 2027?

Household Situation

Practical 2027 HSA Approach

Employer gives HSA money

Use the employer deposit as the base, then decide how much more to add

Recurring prescriptions or appointments

Fund the account for expected medical spending first

High deductible and limited cash reserve

Build an HSA cash buffer before investing

Low current medical use and stable income

Consider saving above the expected spending

Age 55 or older

Use the catch-up contribution if eligibility and cash flow allow

Medicare enrollment is approaching

Review the last eligible month before continuing payroll deposits

Methodology And Sources

Bottom Line